News from the South - Tennessee News Feed

US plans to deport Kilmar Abrego Garcia to a country that’s not El Salvador, prosecutor tells judge

SUMMARY: President Donald Trump’s administration plans to deport Kilmar Abrego Garcia to a “third country” after his release from jail in Tennessee, rather than his native El Salvador, a federal prosecutor told a judge. There is no set timeline for the deportation, and the government intends to comply with court orders. Abrego Garcia, mistakenly deported to El Salvador in March despite a 2019 immigration judge’s order protecting him, faces human smuggling charges in the U.S. His attorneys seek to keep him in Maryland pending trial to prevent deportation. The case remains under judicial review, with a hearing set for July 7.

The post US plans to deport Kilmar Abrego Garcia to a country that's not El Salvador, prosecutor tells judge appeared first on www.wkrn.com

News from the South - Tennessee News Feed

Nashville’s geology has been misunderstood in tunneling talks — including by a Boring Company executive

SUMMARY: The Boring Company plans to build a tunnel connecting downtown Nashville to the airport, but the city’s limestone geology poses challenges. Nashville sits on porous limestone formed during the Ordovician period, making it prone to sinkholes and underground instability. Experts warn tunneling in this karst terrain is hazardous, risking sinkhole formation and disrupting water flow. Studies urge disaster planning due to unpredictable fractured rock and water movement. Local geological data is outdated, complicating risk assessment. Nashville’s climate extremes, including heavy rainfall, could exacerbate these issues. Elon Musk’s company favors fewer pre-project reviews, raising safety concerns amid uncertain environmental impacts.

The post Nashville’s geology has been misunderstood in tunneling talks — including by a Boring Company executive appeared first on wpln.org

News from the South - Tennessee News Feed

Former Mid-South prison could become Tennessee ICE detention center

SUMMARY: A small West Tennessee town is deciding whether to reopen a former Mid-South prison as an ICE detention center. The facility, closed since 2021 after the Biden administration phased out private prison contracts, is owned by CoreCivic. Town leaders will vote on a contract with ICE and CoreCivic to house immigrants. Residents have mixed reactions: some worry about the impact of an ICE facility, while others see potential job opportunities, with CoreCivic promising nearly 240 local jobs and over 3,000 applicants. CoreCivic emphasizes they do not enforce immigration laws but provide care and legal due process.

Town leaders in Mason are set to decide Tuesday whether to reopen a closed detention facility as an Immigration and Customs Enforcement (ICE) site—a proposal that is drawing mixed reactions from residents. READ MORE: https://www.fox13memphis.com/news/residents-divided-on-possible-new-mid-south-ice-facility/article_a4523a44-68c8-4ef3-a0da-b9cf86a2d916.html

ABOUT FOX13 MEMPHIS:

FOX13 Memphis is your home for breaking news, live video, traffic, weather and your guide to everything local for the Mid-South.

CONNECT WITH FOX 13 MEMPHIS:

Visit the FOX13 Memphis WEBSITE: https://www.fox13memphis.com/

Like FOX13 Memphis on FACEBOOK: https://www.facebook.com/fox13news.myfoxmemphis

Follow FOX13 Memphis on TWITTER: https://twitter.com/FOX13Memphis

Follow FOX13 Memphis on INSTAGRAM: https://www.instagram.com/fox13memphis

SUMMARY: Mason, Tennessee, a small town of about 1,300, is deciding whether to approve a contract with ICE and CoreCivic to reopen the West Tennessee Detention Facility, closed since 2021. CoreCivic aims to house immigrant detainees, promising nearly 240 jobs and significant tax revenue for Mason. However, lifelong resident Eloise Thompson and immigrant rights groups oppose the plan, citing community harm and the negative impact of a for-profit private prison. CoreCivic insists it will provide humane care under government oversight and does not enforce immigration laws. A special town meeting Tuesday will finalize the decision amid expected protests.

The post Small West Tennessee town weighs ICE detention contract appeared first on www.wkrn.com

Dragon Bravo fire grows to one of the largest | FOX 5 News

Springfield City Council considers rental inspection program

Florida wildlife officials to decide Wednesday on controversial bear hunt

Scattered storms chances ramp up into the mid-week

Nashville’s geology has been misunderstood in tunneling talks — including by a Boring Company executive

Mitchell Farms: A Mississippi Treasure in Collins

Trump admin may reclassify marijuana: Would that make it legal in the US?

MAP: Where have Austin's homicides occurred in 2025?

Former Mid-South prison could become Tennessee ICE detention center

Shooter kills 3 in a Target parking lot in Austin, Texas, before being captured, police say

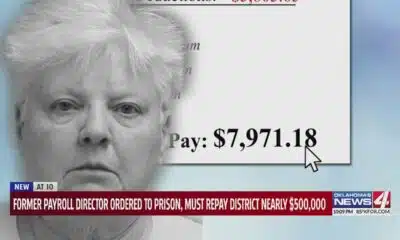

Former payroll director ordered to prison, must repay district nearly $500,000

Two people unaccounted for in Spring Lake after flash flooding

Trump’s new tariffs take effect. Here’s how Tennesseans could be impacted

Jim Lovell, Apollo 13 moon mission leader, dies at 97

Man accused of running over Kansas City teacher with car before shooting, killing her

Tulsa, OKC Resort to Hostile Architecture to Deter Homeless Encampments

Why congressional redistricting is blowing up across the US this summer

Arkansas courts director elected to national board of judicial administrators

Students have been called to the office — and even arrested — for AI surveillance false alarms

Drugs, stolen vehicles and illegal firearms allegedly found in Slidell home

Dragon Bravo fire grows to one of the largest | FOX 5 News

Former Mid-South prison could become Tennessee ICE detention center

Fayette County Schools superintendent on staying safe as school starts up again

South Mississippi schools recognized for reading success

Charter schools in WV say they’ll allow religious vaccine exemptions

Partly cloudy and warm across South Florida, a few scattered showers possible

Mississippi Power donates $350,000 to United Way for customer bill relief amid extreme temperatur…

In Depth with Dan: Answering viewer questions about flesh-eating bacteria, digital licenses

Sports and entertainment store Scheels coming to the metro

Grand Jury records from Epstein case to remain sealed

-

News from the South - Oklahoma News Feed3 days ago

News from the South - Oklahoma News Feed3 days agoFormer payroll director ordered to prison, must repay district nearly $500,000

-

News from the South - North Carolina News Feed6 days ago

Two people unaccounted for in Spring Lake after flash flooding

-

News from the South - Tennessee News Feed5 days ago

Trump’s new tariffs take effect. Here’s how Tennesseans could be impacted

-

News from the South - Texas News Feed4 days ago

Jim Lovell, Apollo 13 moon mission leader, dies at 97

-

News from the South - Missouri News Feed4 days ago

Man accused of running over Kansas City teacher with car before shooting, killing her

-

News from the South - Oklahoma News Feed6 days ago

Tulsa, OKC Resort to Hostile Architecture to Deter Homeless Encampments

-

News from the South - Arkansas News Feed6 days ago

News from the South - Arkansas News Feed6 days agoWhy congressional redistricting is blowing up across the US this summer

-

News from the South - Arkansas News Feed5 days ago

Arkansas courts director elected to national board of judicial administrators